‘This might be a housing bubble,’ Says Dallas Fed Economist—Here’s an Exclusive Look at the Latest Housing Market Analysis

Dallas Federal Reserve

Dallas Federal Reserve

Back in March, economists at the Federal Reserve Bank of Dallas put the real estate industry on high alert when they published a paper titled "Real-time market monitoring finds signs of brewing U.S. housing bubble." It's one thing for Redditors on the r/REBubble board to pontificate about housing bubble theories. But when a Federal Reserve bank engages in bubble talk, that's alarming.

That Dallas Fed paper found that U.S. home prices are once again becoming detached from underlying economic fundamentals. However, if a housing correction comes, they wrote, it's unlikely to cause a 2008-style housing crash. Homeowners are less debt-burdened this time around. Not to mention, the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act eliminated many of the financial products that underpinned the credit-fueled bubble of the 2000s.

Fast-forward to today, and that Dallas Fed report—which used data from the fourth quarter of 2021—is already outdated. The first three months of 2022 was arguably the hottest quarter ever recorded in housing. On Tuesday, we learned the year-over-year home price growth rate hit an all-time of 20.6% between March 2021 and March 2022. While things in April and May finally began to cool down, home prices still remain well above levels hit in the final months of last year.

To see where the U.S. housing market stands now, Fortune reached out to the Dallas Fed. We asked Enrique Martínez-García, a senior research economist at the Dallas Fed, for his thoughts on the housing market and to see if the bank would provide Fortune with an updated analysis. He obliged.

"This might be a housing bubble. The evidence suggests it looks like a housing bubble. A little bit like a duck. It walks like a duck, it looks like a duck, it certainly might be a duck," Martínez-García tells Fortune. While he won't go so far as to call this a housing bubble, he says it's time to "raise awareness to the potential risks [that] housing poses."

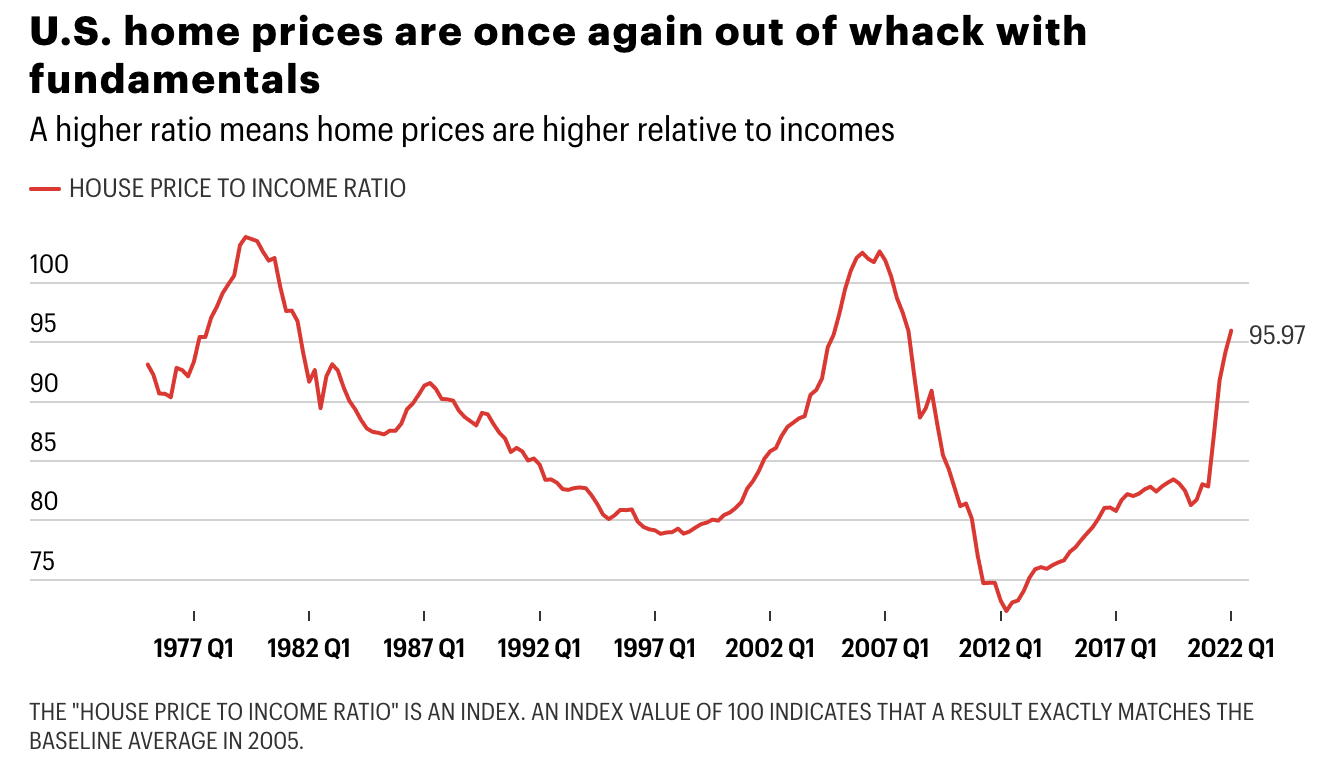

The onset of the pandemic saw mortgage rates plummet to historic lows while remote work allowed home shoppers to buy from, well, just about anywhere. The housing boom set off didn't take long to begin showing signs of "exuberance." That's clear in the house price to income ratio created by the Dallas Fed. It's an index, with the value of 100 indicating a housing market exactly equal to the 2005 baseline year. The finding? In the fourth quarter of 2019, the index sat at 83.1. The Dallas Fed paper found that by the fourth quarter of 2021, the pandemic housing boom had pushed the index all the way to 94.16.

Where do we stand now? In the first quarter of 2022, that house-price-to-income ratio rose to 95.97, the highest reading since the fourth quarter of 2004. It's still a ways off from the 102.64 peak of the housing bubble in 2006, but historically speaking, we've moved into a period where home prices are nearing the limits of what incomes can afford. The last time this happened, home prices eventually snapped back.

Where do we head from here?

Martínez-García notes that this is a time of fighting inflation, with the Federal Reserve already putting upward pressure on mortgage rates. Over the past five months this has sent the average 30-year fixed mortgage rate up from 3.11% to 5.09%, as the Fed works to rein in price growth.

"That's one way to take some air out of housing," Martínez-García says.

As home prices soared during the pandemic, home shoppers were protected, to a degree, by historically low mortgage rates. Now that mortgage rates are back above 5%, borrowers are feeling the full weight of the 36.8% jump in home prices over the past two years. At a 3.11% fixed mortgage rate, a borrower would see a $2,138 payment on a $500,000 mortgage. At a 5.09% rate, that same loan would generate a $2,712 monthly payment. Over 30 years, that's an additional $206,597.

As data rolls in for April and May, it's crystal clear that higher mortgage rates have changed the trajectory of the housing market: We're in slowdown mode. New home sales, existing home sales, and mortgage applications are falling—fast. Inventory is rising again. And Redfin finds the share of sellers cutting list price has spiked to its highest level since 2019.

In Martínez-García's eyes, a slowdown in the housing market is critical. If home price growth decelerates significantly, it'll prevent the Dallas Fed's house-price-to-income ratio from matching the levels it notched in at the height of the ’00s housing bubble.

"If this [the housing boom] goes unchecked ... things could get worse," Martínez-García says. That said, the continued mismatch between housing demand and supply makes it unlikely that slowing would actually cause home prices to drop over the coming year. Indeed, Martínez-García expects home prices (in "nominal" and "real" terms) to notch a slight uptick over the next 12 months.

By: Lance Lambert I Fortune I June 3, 2022