Realtor.com Site Visitor Survey 2025 Q1: Concerns on Recession Are Rising

Highlights

It has been a turbulent year since the start of 2025, marked by a series of tariff announcements, a volatile stock market, and an unclear picture of the U.S. economy—all contributing to uncertainty around the Fed’s next move and, ultimately, the direction of mortgage rates and the housing market.

To better understand whether homebuyers’ sentiments have changed and to grasp the current challenges they face, we analyze information collected from the Realtor.com Site Visitor Survey by focusing on three key questions:

Buyer economic perceptions

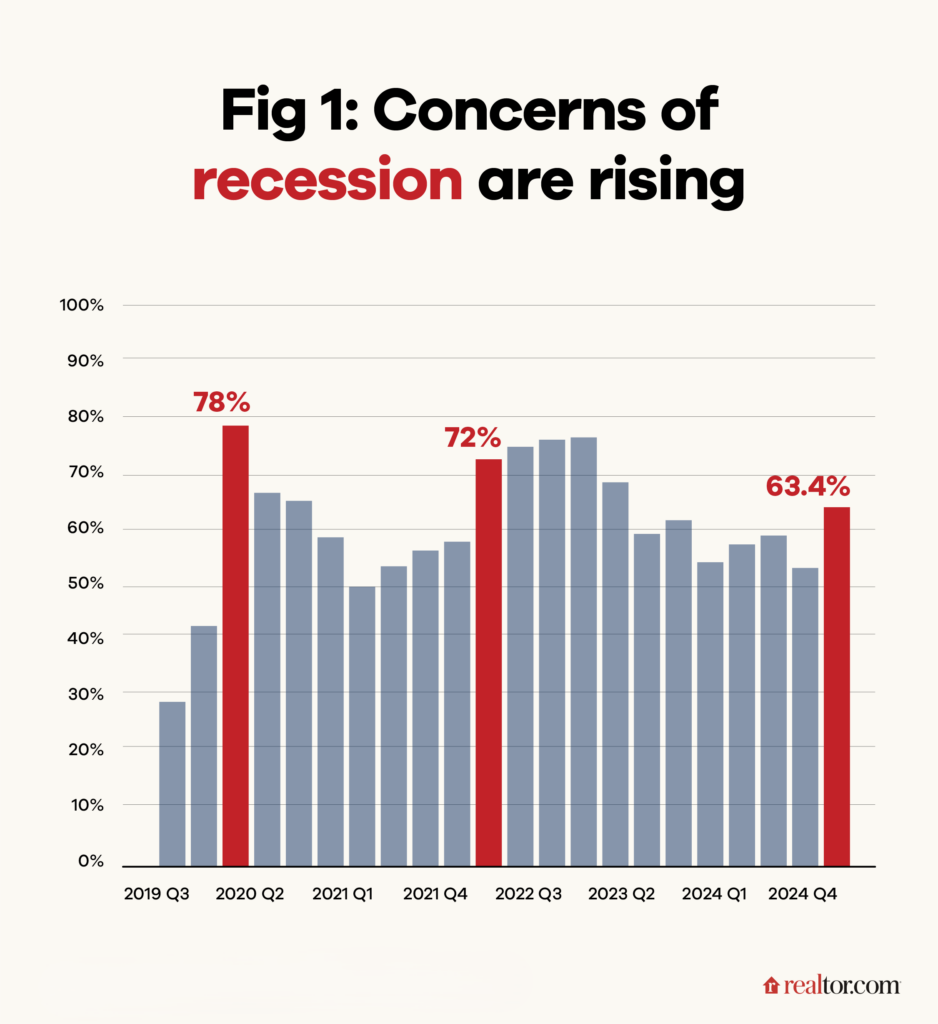

Recent homebuyers have grown increasingly concerned about the U.S. economy, with current sentiment ranking among the most pessimistic periods in recent years. In the first quarter of 2025, 63.4% of home shoppers believed a recession was likely within the next year, as a wave of tariff announcements beginning in February fueled fears of a global trade war and triggered heightened market volatility. This marks the third-highest period of economic concern, following the 78% peak in 2020Q2 that coincided with the trough of economic activity following the onset of the pandemic and the sustained 70%+ levels from 2022Q2 through 2023Q1, when the Federal Reserve aggressively raised interest rates, sparking several bank failures and negative news coverage even as the economy avoided a recession.

Already, consumer surveys have shown declining expectations for better personal financial situations and higher concern about potential job loss. In fact, the expectations component of consumer confidence fell to its lowest reading since October 2011 in the April preliminary data.

Looking ahead, concerns about the U.S. economy are expected to remain elevated in 2025Q2 due to factors such as ongoing high interest rates, continued stock market volatility, and global trade tensions unless there is significant de-escalation from current proposals. These elements could further dampen consumer confidence and economic growth, raising fears of a potential slowdown.

How might a recession influence homebuying decisions?

In 2025Q1, 3 in 10 (29.8% of) surveyed homebuyers said a recession would make them at least somewhat more likely to purchase a home, while 15.8% indicated they would be less likely to buy after a recession hits. This reflects a common dynamic where some buyers see a downturn as an opportunity. If the economy enters a recession, the Federal Reserve may respond by lowering interest rates to stimulate activity, potentially putting downward pressure on mortgage rates and easing affordability concerns. As a result, buyers—especially those with limited down payments—might view a recession as a more favorable time to enter the market.

While some buyers adjust their strategies based on the economic climate, more than half of respondents (54.4%) said a recession would have no impact on their decision to buy. Many of these active home shoppers might already be financially secure, motivated by personal or lifestyle needs, and focused on long-term goals. For them, short-term economic uncertainty is likely less important than the perceived long-term value of homeownership.

What else affects buying decisions?

While homebuyers might differ in their views on the timing of a recession and their responses to it, one persistent concern stands out: limited housing inventory.

In 2025Q1, 44.3% of homebuyers reported being unable to find a home that met their needs—a challenge that has consistently ranked as the top barrier to purchasing in our survey data dating to 2019. Although listing activity has rebounded and today’s buyers have more fresh options compared with one year ago, overall active for-sale housing inventory remains 16.3% below typical levels seen from 2017 to 2019, indicating the market still has ground to make up.

Meanwhile, 36% of surveyed homebuyers identified budget constraints as a key barrier to homeownership. This concern could become even more pressing in the coming quarters amid uncertainty over the economic impact of tariffs. If tariffs drive up import costs and fuel inflation, this could reduce the amount of housing budget available. Further, the Federal Reserve might respond by raising interest rates, or keeping them higher for longer, to keep inflation in check—leading to higher mortgage rates than otherwise. In light of this uncertainty, it is increasingly important for homebuyers to stress-test their budgets and plan for a range of financial scenarios.

In addition, concerns about mortgage qualification (8.2%) and poor credit scores (13.5%) became more prominent in Q1 2025. This trend is not surprising, as lenders often tighten credit standards during periods of economic uncertainty or market volatility to mitigate risk. Stricter requirements might include higher credit score thresholds, larger down payments, and more rigorous documentation of income and employment. Supporting this, a February 2025 survey by the Federal Reserve Bank of New York found that consumers increasingly expect greater difficulty and higher rejection rates when applying for credit, including home loans. Further, changes in student loan repayment requirements and credit reporting are also expected to begin to affect credit scores in early 2025 with 9 million student loan borrowers expected to face declines in credit standing. This could be a factor for some consumers.

On the bright side, only 7.7% of surveyed home shoppers cited overbidding as a concern in 2025Q1—down from 10.4% during the same period last year. This points to a less competitive market environment, where buyers might be feeling less pressure and stress. The trend aligns with broader market conditions, including increased inventory, relatively stable prices, and longer days on the market—all of which suggest a slower-paced housing market.

Methodology: Background and context

To better understand the sentiment and experiences of buyers, sellers, and renters currently on the market for homes, the Realtor.com economics team conducts a randomized survey of visitors to listing detail pages on the site, the Site Visitors Survey. Respondents are asked about the reasons they’re visiting the site, how they’ve been engaged with the housing market, and how they feel that current market conditions are affecting their behavior. The survey was first launched in the fourth quarter of 2019, and this report focuses on results reported from shoppers in 2025Q1.

Surveys are administered randomly to visitors on Realtor.com. For this report, we consider only respondents who indicate that they are homebuyers. Weights are calculated by computing the share of survey respondents falling into categories based on age and adjusting these proportions to match the share of all visitors to Realtor.com and similar online real estate marketplaces segmented by age.

By: Jiayi XuI Realtor.com I May 20, 2025