Downtown Aspen Assets on the Line in Souki Lender Dispute

The saga involving a group of lenders battling a well-heeled Aspen family over the family’s local property holdings, gas company stock, real estate firm and massive luxury ranch is told through public records, emails, affidavits and court-hearing transcripts.

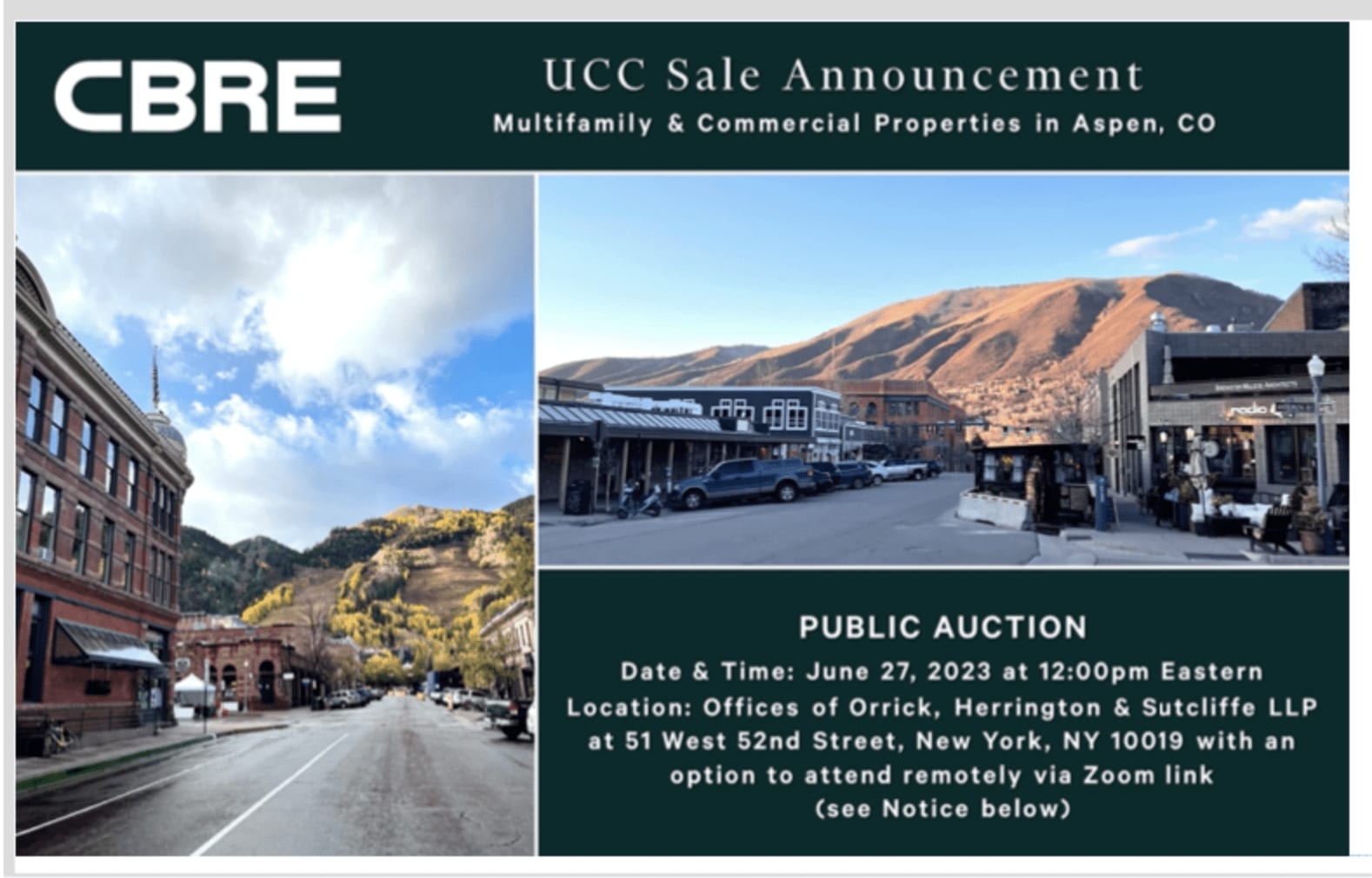

Those documents show that the dispute doesn’t end with the lenders’ attempted foreclosure on Aspen Valley Ranch. The assets owned by Ajax Holdings, which is controlled by the Souki family and affiliates, also are on the line. The lenders have hired Dallas-based commercial property firm CBRE to solicit bidders and administer a public auction set for the end of the month, according to court records.

Ajax Holdings’ assets include well-established local real estate franchise Coldwell Banker Mason Morse and “collateral consisting of multifamily, retail condo and office properties in Aspen, Colorado,” according to public notices and marketing materials for the sale.

The Soukis’ Aspen Valley Ranch is a collection of luxury custom-built homes, a fishing and boating pond, a historic barn converted into a clubhouse decked out with a dining area and recreation center, an eight-horse barn, and other amenities on an 800-plus-acre swath of land in Woody Creek.

The looming sales would come after family patriarch Charif Souki pledged Aspen Valley Ranch, his 25 million shares of stock in a liquified natural gas company he co-founded, his luxury sailing yacht and the assets of the Souki Family 2016 Trust and Strudel Holdings LLC as collateral on a combined $120 million in loans he received in 2017 and 2018. (An initial $50 million loan was paid down by $30 million, before the lenders increased the loan by another $70 million in 2018.) The Souki Family 2016 Trust and Strudel Holdings are the 50-50 owners of Ajax Holdings.

In a lawsuit introduced March 6 in the commercial division of the New York Supreme Court and in sworn affidavits filed as part of the case, Souki and his lawyers contended the lenders were made whole — between their selling Souki’s 25 million shares of stock in the liquified natural gas company Tellurian earlier this year and their seizing Souki’s prized sailing yacht last year and putting it under contract for sale for an undisclosed amount. The lawsuit seeks to prevent the sale of Ajax Holdings.

Souki’s lawyers on March 24 filed an amended complaint that said the lenders “have no further right to exercise loan remedies” and because “they have already foreclosed on collateral sufficient to extinguish Souki’s debt in full, they have no legal right to foreclose on further collateral.”

Souki is seeking a permanent injunction to stop the sale of Ajax Holdings in New York after a judge on May 1 denied his motion for a preliminary injunction. The lending group is likely to enter a response by June 6 to the complaint, which seeks a court order that would discharge the debt and a permanent injunction that would halt the sale.

If Souki fails in his legal attempt to halt the auction, the Ajax Holdings sale is scheduled to take place June 27 in New York City. The Aspen Valley Ranch foreclosure auction, if approved by a Pitkin County District Court judge, is scheduled for July 26.

The sales are being handled differently but have the same endgame for the lenders, which is to foreclose on Souki’s assets that were pledged as collateral. Based on a statement from a Souki lawyer at the May 1 court hearing, the bottom line in the impasse is $128 million, which represents $90 million in principal and the rest interest, according to court records.

“That was never the balance at any given point in time, but that is the total,” said Houston lawyer Timothy McConn, who is Souki’s counsel, at a May 1 court hearing in New York. McConn, whose remarks were gleaned from a hearing transcript, noted the total amount owed is calculated “when you add up all the interest that [the lenders] say has accrued.”

Souki’s lawyers, including McConn, did not respond to messages for this story.

Lawyers for the lending group — Nineteen77 Capital Solutions of New York, Bermudez Mutuari Ltd. of the Cayman Islands, Chicago-based UBS O’Connor LLC and Delaware-based Wilmington Trust National Association — have argued that the sales are proper, and they have tried with no success to work out a deal with Souki. They also did not return messages for this story.

The Ajax Holdings assets are being put up on what’s called a Uniform Commercial Code (UCC) sale, which can be triggered when there is a default on a bridge loan where partnership interests are pledged as collateral.

That is what’s happening in New York, because Souki entered into bridge agreements for the loans with the lenders in May 2020. The agreements expired March 31, 2021. As such, the lenders are exercising their right under federal UCC laws to sell the partnership or equity interests in Ajax Holdings.

Select details about the sale are disclosed in an investor solicitation email, which is presented as evidence in Souki’s New York litigation. According to the solicitation’s “investment highlights,” Ajax Holdings’ assets for sale include but are not limited to “several commercial and mixed‐use properties (retail, multifamily & office) located in downtown Aspen, Colorado, a world‐class mountain town and year‐round destination.” Also, the solicitation says Ajax Holdings’ “commercial properties’ high street retail is situated in downtown Aspen — a location that is tailored to foster successful boutique retail & restaurant operations.”

The email does not identify the properties by address or name. According to property records, Ajax Holdings’ assets include three parcels on the Hyman Avenue pedestrian mall and the building at 514 E. Hyman Ave, which houses the Mason Morse real estate firm. An affiliate of Ajax Holdings, Durant AH, owns just over 4,000 square feet of commercial space in the Aspen Square Hotel, which is occupied by Performance Ski.

While the total estimated value of the Ajax Holdings assets does not appear in the records reviewed by Aspen Journalism, the combined free-market value of Aspen parcels known to be controlled by the company is $60.7 million, according to the Pitkin County Assessor’s Office. That does not include the value of the real estate brokerage, and may not be inclusive of all properties controlled by Ajax Holdings.

Souki family spokesperson Karim Souki, Charif’s son, did not respond to questions about the two pending auctions. Will Herndon, managing director of Ajax Holdings and president of Mason Morse, also did not respond to messages for this story.

Charif Souki emphasized his concerns regarding the sale of Ajax Holdings in a signed affidavit dated April 28, which is an exhibit in his New York court action.

Although New York is not the jurisdiction for the foreclosure action on Aspen Valley Ranch — which is in Pitkin County — Souki’s affidavit said, “I fully intend to keep the ranch in the family for years to come. Similarly, Ajax Holdings took 10 years to build, it contains a unique set of real estate assets” … with “several hundred employees whose livelihoods would be at risk if defendants are permitted to sell it to a prospective buyer.”

Several Mason Morse brokers said they were unaware their firm was for sale.

Souki’s affidavit depicted a bleak scenario in the event of the two sales taking place: Mason Morse employees would lose their jobs and Souki would lose his residence at Aspen Valley Ranch, which was developed in the mid-2010s into a collection of homes for a family compound. The Soukis bought the property in August 2013.

“To permit the sale of these unique assets before the issues in this case are fully and finally litigated would render me homeless, strip my family of its privately held business, cause my children and hundreds of other Ajax Holdings employees to become unemployed,” Souki said in the April affidavit.

Souki initiated a second attempt for a preliminary injunction — not to stop the sale of Ajax Holdings but to allow his participation in it — in a May 23 filing in New York court.

The filing argued that the lenders were excluding Souki from any chance to be involved in the New York sale of Ajax Holdings. Souki’s lawyers withdrew the motion May 25 after the lenders’ lawyers, in a letter to the judge May 24, countered that Souki can participate in the auction “and of course may exercise his right of redemption at any time by repaying the loan balance (which would obviate the foreclosure sale).” More than 180 potential bidders had expressed interest in the Ajax Holdings sale as of May 24, the lawyers stated.

CBRE, the company administering the sale for the lenders, did not respond to a message concerning details of the sale, which has been publicly noticed in legal advertisements published in newspapers in both Aspen and Baton Rouge, La.

Through a limited liability company called AVR AH, Souki and investors acquired Aspen Valley Ranch for $27 million nearly a decade ago from Alpine Bank, which had foreclosed on the property in December 2012.

The sale included a main house with five bedrooms and five baths and the property’s historic features — as well as entitlements to build 14 luxury homes. Souki went onto develop the gated property into “more than 60,000 feet of improvements including approximately 34,397 square feet of residential property with eight custom homes, complete with 31 beds, 31 baths and five partial baths, just under 14,000 square feet of common facilities, and more than 10,000 square feet of operational facilities. Additionally, the ranch has more than 80,000 square feet of unrealized, residential development potential,” said a press release dated May 22, 2020.

The release trumpeted the $220 million for-sale listing of the gated community of Aspen Valley Ranch. A statement from Souki explained that “for us, it is time to move onto the next project.”

Around the same time the sale was announced, Souki, who had amassed a fortune as a pioneer in the field of liquified natural gas (LNG), was seeing the value of Tellurian plummet.

Souki owned 25 million shares of Tellurian stock, which he received in 2016 in exchange for investing $25 million into the startup, making him the company’s largest shareholder. Tellurian shares were trading from $7 to $8 in early 2020. Yet, the global financial meltdown, triggered by the COVID-19 pandemic and resultant lockdowns in March 2020, sent Tellurian shares spiraling below $1, Souki’s lawyers noted.

“In early 2020, this becomes a problem. And the reason it becomes a problem is because two very significant things happen in the market, and it severely impacted the Tellurian stock cost,” said McConn at the May 1 hearing in New York.

The first blow came when an India-based LNG company called Petronet withdrew its commitment to invest $2.5 billion in an LNG terminal facility, known as Driftwood, that Tellurian had planned to develop in Lake Charles, La., according to McConn. (Tellurian announced in April that it had found a buyer for the 800 acres of Louisiana land tapped for the facility; Tellurian will lease back the land.)

“Petronet was going to be one of the primary customers of Tellurian, and in February of 2020, they announced that they were backing away from the table. That sent the stock price down very significantly,” McConn said. “The second thing that happened was in March of 2020, COVID occurred, and that just blew up the oil and gas markets around the world. That also strained very heavily — strained the Tellurian stock price.”

As the value in Tellurian shares reeled, the lending group grew worried about their financial picture: They had floated $75 million to the Tellurian company in May 2019 — Souki alleged in his New York lawsuit that he was kept in the dark about the loan — in addition to the $120 million they had loaned Souki from April 2017 to March 2018.

They also had secured the 25 million shares as collateral on Souki’s loans and exercised their contractual right to take control of the shares on May 5, 2020, according to court records.

Meanwhile, the lending group, believing Souki could “right the ship” at Tellurian, persuaded him to return to the helm. On June 22, 2020, Souki became executive chair of Tellurian’s board of directors, making him the face of the company and actively involved in daily operations.

It was Souki’s understanding — through a verbal, not written, agreement with the lenders — that if Tellurian repaid the loan, then “they would not touch (Souki’s) stock, his Tellurian stock that was pledged as collateral,” McConn said. Souki also urged the lenders not to exercise their right to sell his shares and wait until Tellurian started meeting milestones that improved the company’s value, according to his lawsuit.

On Souki’s watch, Tellurian made good on the $75 million loan in March 2021, but the lending group soon ramped up the pressure on him to start repaying his debt when two of Souki’s bridge-loan agreements had expired. The lenders asked for an upfront payment of $5 million, with the remaining balance due Oct. 30, 2021, according to Souki’s legal team. Souki rejected the offer.

“So, the only loan that’s left outstanding are Mr. Souki’s personal loans, which he was told they would be very flexible in how they would deal with it,” McConn said at the May 1 hearing. “And they wouldn’t touch his Tellurian stock until after Tellurian achieved these milestones. Well, that promise went out the window.”

Although the lenders had seized control of Souki’s stock, by May 20201 they were demanding that he sell it. Souki refused, and the disagreement spilled into mid-2022, when the lenders threatened to foreclose on Aspen Valley Ranch. They held off on the ranch foreclosure, but in December, they seized Souki’s prized 98-foot sailing yacht; it is under contract for an undisclosed sum, according to court documents.

Tellurian stock, which had bounced back to $5 to $6 per share the previous year, was trading below $2 in February, after the company faced setbacks brought on by delayed or canceled contracts on the Driftwood project in Louisiana. February also was when the lenders started to dump the Tellurian shares seized from Souki.

“At the beginning of this year, in February of ’23,” McConn said at the hearing, “they then seized the Tellurian shares. They already had exclusive control over the shares. They took a step in seizing the shares, actually moving, directing the broker to physically — not physically, but electronically — move the shares of Mr. Souki’s account to the defendants’ account. Now, this is just a ministerial act because, as I’ve said a few times now, at that point they controlled the shares. But that was the first time, in February of ’23, that they actually took their own advice and used the exclusive right that they had and went ahead and started selling the stock.

“Yet, for whatever reason, they dumped his shares on the market when it was at a two-year low, and the trading volume was such that if the executive chairman’s (shares) gets dumped into the mix, it’s going to move the price dramatically,” McConn said at the hearing. “And yet they did it anyways. And the very first day, they dumped almost 2 million of his shares on the market, roughly 15% or so of the total volume for that day. It drove the price down by 10%, not surprisingly.”

Over the course of the next six weeks, the lenders sold all of Souki’s 25 million shares.

“For the 25 million shares that they could’ve received $158 million for back in April of 2022, they received $37 million,” McConn said, noting that although it was too late for the court to stop the share sell-off, it still had the power to prevent the sale of Ajax Holdings.

The figure for the sale of the shares was actually “approximately $35 million,” lawyer Darrell Cafasso said on the lender’s behalf at the May 1 hearing.

“We have not recovered anything else since, and sitting here today, Mr. Souki still owes almost a hundred million dollars on these loans,” Cafasso said, according to the transcript. “Those, your honor, are the undisputed and controlling facts, and everything else plaintiffs say in their affidavits about supposed oral promises, negotiations, expectations, is legally of no moment.”

Cafasso also suggested that Souki’s contention that his entire debt should be eliminated because the lenders mistimed the selling of the shares was conveniently made with the benefit of hindsight.

“At the end of the day, your honor, plaintiffs are just using hindsight to cherrypick a few dates and argue that we could’ve timed the market better, but that’s not the law, your honor,” he said. “The mere fact that a greater amount could’ve been obtained if we sold at a different time, that’s not enough to establish commercial unreasonableness.”

Cafasso later said that “with respect to the Tellurian shares, your honor, here are the undisputed facts. We sold the shares. We didn’t dump them on a single day. We sold them over the course of two months, from February 8th to April 5, 2023, on the New York Stock Exchange.”

Siding with the lenders at the May 1 hearing, Justice Andrea Masley said there was not sufficient evidence for her to find that they were “commercially unreasonable” by selling the shares, which factored into her decision to rule against the preliminary injunction.

The lending group “can’t just do anything they want,” said Masley. “That’s true. They have to do it in a commercially reasonable way. But I just don’t have before me enough facts to find that it is more … likely than not that it was commercially unreasonable to sell the stock when they sold it.”

According to the lending group’s foreclosure papers filed on Aspen Valley Ranch, two residential lots that sold in 2021, as well as two homestead lots (for full-time residency only), are excluded from the action.

A limited liability company called Beyond the Beach paid $31.5 million for a 4,700-square-foot home on the ranch’s 45-acre Lot 8 in October 2021. Three Dolphins acquired Lot 4, also with a home (5,069 square feet on 35 acres), for $15.5 million in August 2021.

Excluding those properties, the ranch has a free-market value of approximately $100 million, according to third-party appraisals cited in the New York litigation.

Aspen Valley Ranch has been marketed as a luxury vacation retreat with full amenities and services. Souki’s household is the family’s only one at the ranch for the moment. Only Souki lives on the ranch these days, he said in a sworn statement.

“There was only one reason why, in early 2021, I asked my children to move out of their houses on the ranch and to rent some of the houses and market them for sale — my need to satisfy my obligation to my lenders,” Souki said in the April 28 affidavit. “I never stopped wanting the ranch to serve as my and my family’s home, but selling the ranch was the only viable path to satisfying a large portion of the debt due to the restrictions on my ability to sell my Tellurian shares. And now that my obligation has been satisfied based on defendants’ misconduct and defendants are attempting to foreclose, I am no longer listing the ranch properties for sale and I am not actively marketing them. We plan to keep the ranch in the family.”

Souki was born in Egypt, and in 1996, he founded Houston-based LNG company Cheniere Energy, which he left in 2015. He also started the Aspen restaurant called Mezzaluna, which he no longer owns.

Rick Carroll I Aspen Journalism I June 4, 2023