A housing bubble is brewing—but not like 2008—says Federal Reserve Bank of Dallas

Fortune

Fortune

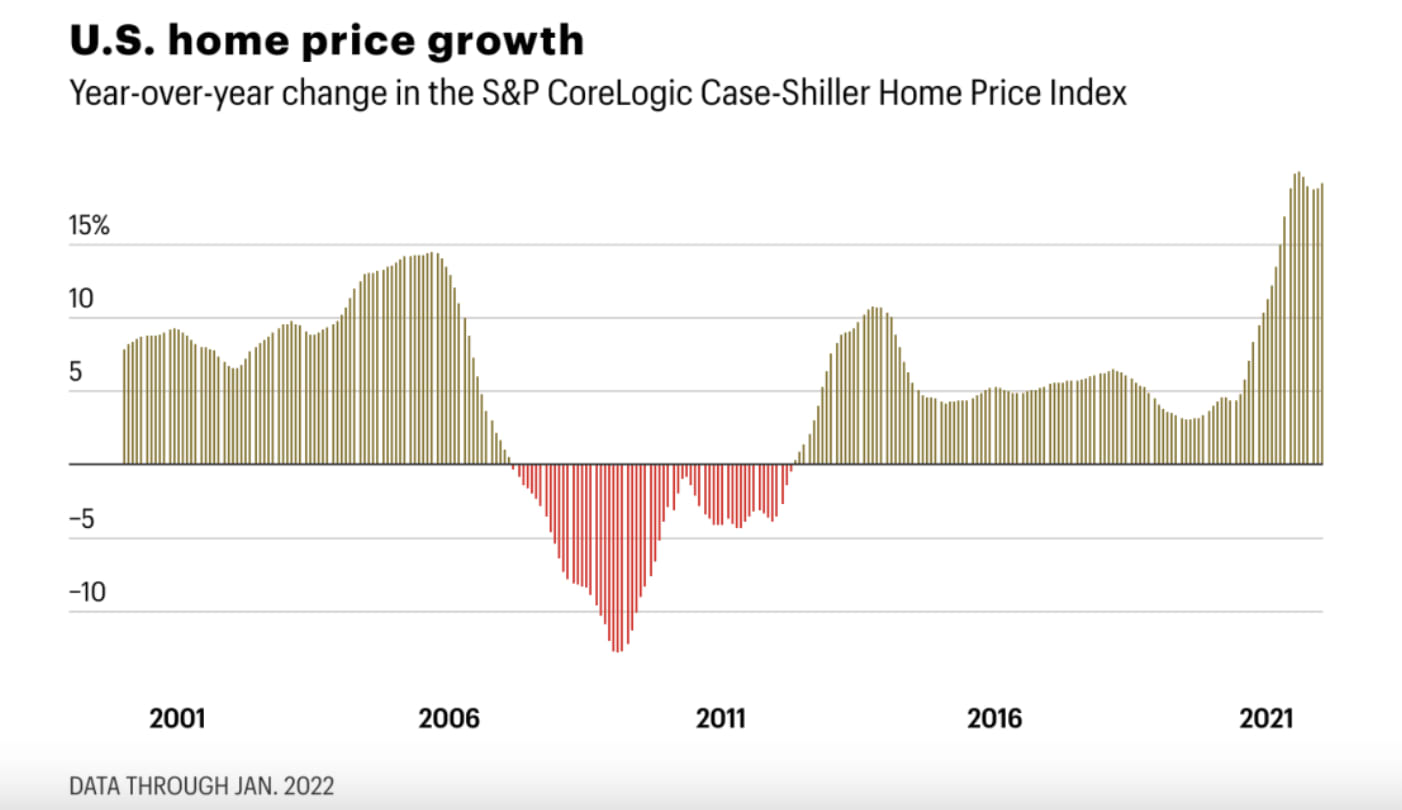

Home shoppers who paused their search last year, in hopes that 2022 would be friendlier, aren't feeling great: We learned on Tuesday that year-over-year U.S. home price growth accelerated to 19.2% in January. That's up from the 11.3% uptick posted at the same time last year. The latest jump is also well above the peak annual rate (14.5%) posted in the lead-up to the 2008 housing bubble.

That stubbornly hot housing market is beginning to raise more eyebrows. Look no further than a paper published this week by the Federal Reserve Bank of Dallas titled "Real-time market monitoring finds signs of brewing U.S. housing bubble." The Dallas Fed researchers came to that conclusion after comparing U.S. home prices to underlying economic data.

"Our evidence points to abnormal U.S. housing market behavior for the first time since the boom of the early 2000s. Reasons for concern are clear in certain economic indicators...house prices appear increasingly out of step with fundamentals," wrote the Dallas Fed researchers.

Amid the pandemic, historically low mortgage rates and a demographic wave of first-time millennial homebuyers helped to spur the ongoing housing boom. However, that alone can't explain the explosion in home prices. Another factor, argues the researchers, could be "fear-of-missing-out"—or home shoppers who think they could be left behind if they don't rush into the market. That's concerning, considering that FOMO home buying was a key ingredient in the last housing bubble.

The good news? While researchers at the Dallas Fed see a bubbly housing market, they don't think we're headed for a 2008-style crash. For starters, households are in much better shape today. Back in 2007, 7% of U.S. disposable personal income was going towards mortgage debt service payments. At its latest reading last year, that figure was just 3.8%.

"Based on present evidence, there is no expectation that fallout from a housing correction would be comparable to the 2007–09 global financial crisis in terms of magnitude or macroeconomic gravity. Among other things, household balance sheets appear in better shape, and excessive borrowing doesn’t appear to be fueling the housing market boom," writes the researchers.

Industry insiders are hoping that spiking mortgage rates—with the average 30-year fixed mortgage rate climbing from 3.11% to 4.42% over the past 12 weeks—can help to tame runaway home price growth before prices get so high it leads to a bursting bubble.

"If rates rise above 5% you will price buyers out of the market... The higher rates could also discourage investor activity, which accounts for a large portion of home sales today," Devyn Bachman, vice president of research at John Burns Real Estate Consulting, told Fortune earlier this week.

Back in 2006, mortgage rates quickly shot up. Those higher rates—at a time when many households had variable mortgage rates—ultimately sped up the demise of countless subprime mortgages and set the stage for the inevitable 2008 financial crisis. This time, in theory at least, rising mortgage rates should play out differently. While it will certainly deter some would-be buyers from entering the market, it would have little impact on homeowners. These days, around 99% of mortgages have fixed rates.

By: Lance Lambert I Fortune I March 30, 2022